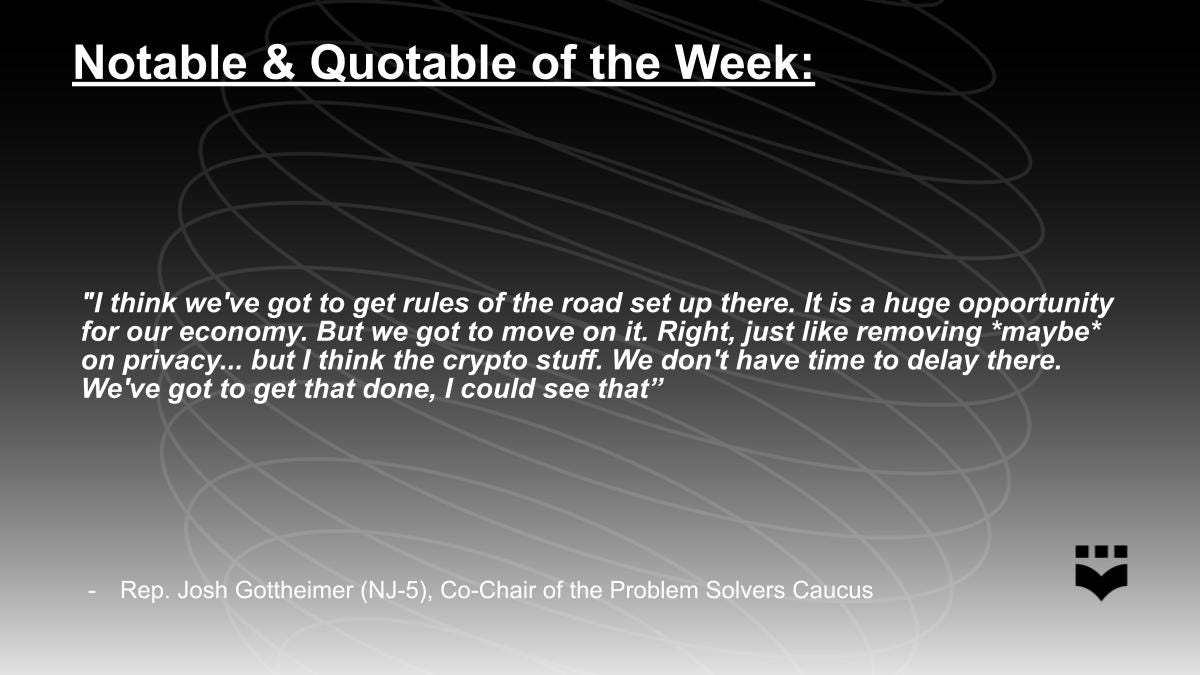

Coinbase Files Lawsuit Against SEC and FDIC; Administrative Proceedings Limited by Supreme Court; Motions for Summary Judgement in LEJILEX

Coinbase Files Lawsuit Against SEC and FDIC

What happened?

Last week, History Associates Incorporated filed lawsuits, on behalf of Coinbase, against the Securities and Exchange Commision (SEC) and Federal Deposit Insurance Corporation (FDIC) to procure documents under the Freedom of Information Act (FOIA). Coinbase is seeking SEC documents regarding “closed investigations to shed light on how the SEC views its newfound, sweeping (and unlawful) authority” over digital assets like Ethereum. Coinbase is also requesting that the FDIC provide copies of letters sent to financial institutions in which the “FDIC requested [the financial institutions] indefinitely pause their crypto-related activities.” After filing the two complaints, Coinbase Chief Legal Officer Paul Grewal posted on X, “This is no way to regulate. And this is no way to operate a transparent government. Today we demand better from our financial regulators.”

What does this mean?

FOIA requests aim to provide the public with insight into federal agencies and help to hold agencies accountable. In this case, both the SEC and FDIC have demonstrated their aggressive positions against digital assets, and Coinbase seeks to reveal the internal deliberations and conversations that formed those policies.

Administrative Proceedings Limited by Supreme Court

What happened?

Last Thursday, the Supreme Court issued its opinion in Securities and Exchange Commission v. Jarkesy. The court held that the Seventh Amendment requires a jury trial when the government or its agencies seek civil penalties for securities fraud. Prior to this decision, the SEC could choose between bringing an enforcement action related to securities fraud against a defendant in federal court or adjudicating the matter internally by having a hearing in front of its own administrative law judges.

What does it mean?

After this decision, targets of SEC enforcement actions seeking civil penalties can insist on a jury trial in federal court and will have the procedural protections guaranteed by the Seventh Amendment. In other words, there will be greater judicial oversight of such cases, and agencies will not be able to act as both the judge and fact-finder in this context going forward.

Motions for Summary Judgement in LEJILEX

What happened?

Last week, motions for summary judgment were filed by both sides in the case brought by the digital asset trading platform, LEJILEX, and the Crypto Freedom Alliance of Texas (CFAT) against the SEC. As a reminder, LEJILEX and CFAT are seeking a declaratory judgment that sales of digital assets should not be considered securities transactions under federal law, and should not require LEJILEX to register with the SEC.

In the SEC’s motion for summary judgment, the SEC argues that the court lacks jurisdiction over the case, the complaint does not state a valid claim, and the relief sought would interfere with the SEC’s enforcement duties. The SEC maintains that whether a digital asset transaction is a securities transaction depends on the specific facts and circumstances, as outlined in the Howey test. The SEC’s motion also argues that plaintiffs have not provided sufficient facts to prove that digital asset transactions can never be securities transactions and urges the court to dismiss the complaint.

In plaintiffs’ motion, they argue that the SEC’s regulatory approach far exceeds its statutory authority and is not justified by existing securities laws. Plaintiffs assert that the LEJILEX trading platform does not facilitate securities transactions and should not be subject to SEC regulation. They claim that the SEC’s actions are creating undue burdens and uncertainty for businesses operating in the digital asset space. Plaintiffs’ motion also emphasizes the need for clear and specific guidelines from the SEC regarding the classification of digital assets.

What does this mean?

Because this case asks the court a purely legal question, no fact discovery is being pursued by either party and the case has moved quickly to summary judgment. Now that both sides have filed their initial motions, they will next write an opposition to their opponent’s motion and then have a chance to reply in further support of their own motion. The court will rule only after all briefing is filed, meaning we are likely to receive a final decision on the merits in 2025.

For a detailed outline on the implications of this case, check out DEF’s blog post.

One More Thing: On Friday, the IRS published finalized text for its “broker” rulemaking. The final rules did not include rules pertaining to DeFi, which the IRS says will come in the future. In the coming weeks, DEF will break down what this all means and what we will be looking out for if the IRS does publish additional rules related to DeFi.

Please note that we will not be publishing a weekly update the week of July 8th, we will be back on the 15th. Have a nice Fourth everyone!